Published by Upcyclea | Singapore Resources | Built Environment Decarbonisation

The Disclosure Gap That Green Finance Is About to Close

Singapore’s real estate investment market has matured rapidly in its engagement with environmental, social, and governance (ESG) frameworks. The Singapore Exchange (SGX) sustainability reporting requirements, the Monetary Authority of Singapore’s (MAS) green finance initiatives, and the alignment of Singapore’s major financial institutions with international frameworks including TCFD, GRI, and GRESB have created a disclosure environment that increasingly demands verified, auditable environmental performance data rather than narrative commitments.

In this environment, a critical disclosure gap is becoming commercially significant: the vast majority of Singapore’s real estate portfolios can report on operational energy consumption and the resulting Scope 2 carbon emissions with reasonable accuracy. Very few can report with any rigour on the embodied carbon embedded in their physical assets — the carbon that was emitted when those buildings were constructed, and that is now a permanent part of their environmental profile whether documented or not.

This gap matters because investors, regulators, and the green finance market are moving toward whole life carbon accounting. The 2025 Built Environment Decarbonisation Technology Roadmap developed by BCA and SGBC identifies embodied carbon transparency as a foundational requirement for Singapore’s built environment decarbonisation. The Green Finance Industry Taskforce (GFIT) and MAS taxonomy for sustainable finance are developing frameworks that will increasingly require Scope 3 carbon data — including embodied carbon — for buildings to qualify as sustainable investment assets. Asset managers who build embodied carbon data capability now are not ahead of a trend. They are preparing for a requirement.

Scope 3 and the Built Environment: Why It Matters for Real Estate

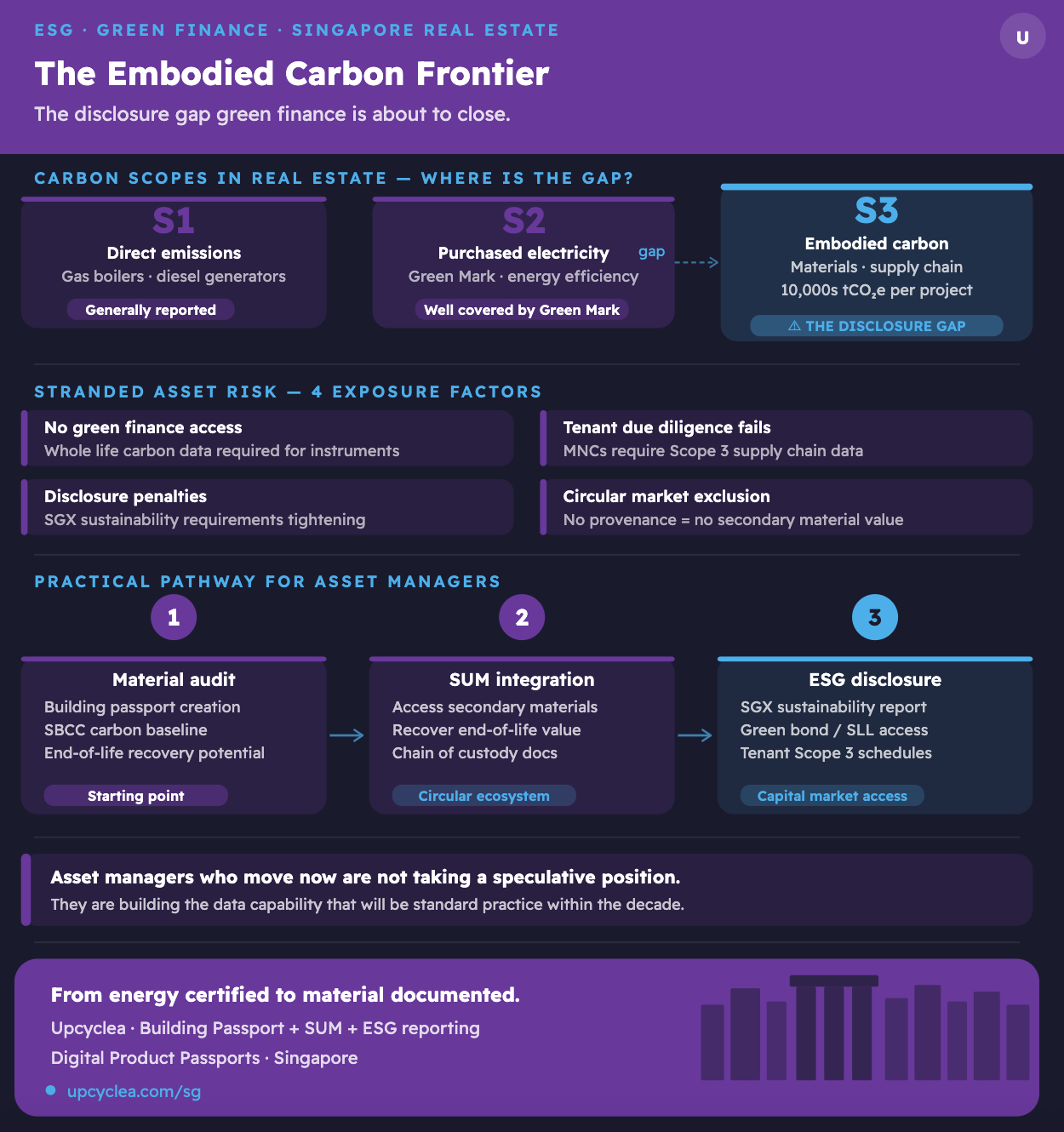

The carbon emissions relevant to real estate investment fall across three Scopes under the GHG Protocol. Scope 1 covers direct emissions from on-site combustion — gas boilers, diesel generators. Scope 2 covers indirect emissions from purchased electricity — the dominant category for most Singapore commercial buildings, and the one most directly addressed by the Green Mark energy efficiency requirements and the progression toward renewable energy under the Singapore Green Plan 2030. Scope 3 covers all other indirect emissions across the value chain.

For real estate owners and developers, the most material Scope 3 category is typically Category 1: purchased goods and services — in practice, the embodied carbon of construction materials. This is the carbon emitted by the concrete manufacturer, the steel producer, the glass fabricator, the aluminium extruder, and every other supplier in the construction value chain before a single brick is laid on site. For a major commercial development in Singapore, this upstream Scope 3 footprint can run to tens of thousands of tonnes of CO₂ equivalent — a carbon liability that is currently invisible in almost all real estate portfolio carbon accounts.

As SGBC has observed, demand for verified Environmental Product Declarations (EPDs) is growing precisely to support the focus on whole life carbon and the pursuit of net zero targets. EPDs allow specifiers and investors to understand the carbon profile of individual materials. Building passports aggregate this data into an asset-level carbon account. Portfolio-level aggregation across documented assets creates the Scope 3 disclosure that institutional investors and green finance providers are beginning to require.

The Carbon Stranded Asset Risk

The concept of stranded assets — buildings whose value is impaired by climate-related physical or transition risks — is well-established in European real estate markets and increasingly relevant in Singapore. The “carbon sieve” problem, where buildings with poor energy performance face regulatory pressure, tenant flight, and capital market exclusion, is already influencing asset allocation decisions among Singapore’s more sophisticated institutional investors.

The embodied carbon dimension of stranded asset risk is less immediately visible but structurally significant. As whole life carbon accounting becomes standard — and the 2025 roadmap makes clear that Singapore intends to move in this direction — buildings without documented material profiles will face growing disclosure penalties. They cannot demonstrate embodied carbon performance. They cannot access green finance instruments that require verified whole life carbon data. They cannot respond to tenant due diligence requests for Scope 3 supply chain data. And they cannot participate in circular material markets that require provenance documentation for recovered components.

The buildings that are most exposed to this transition risk are precisely those with the highest embodied carbon profiles: concrete-intensive structures built without low-carbon specification, facades assembled without EPD-documented materials, fit-out installed without any material traceability. These are also, statistically, the most common buildings in Singapore’s current stock. The transition risk is therefore systemic — and the mitigation strategy is documentation, specification improvement, and connection to circular material infrastructure.

Green Finance Instruments and What They Now Require

Singapore’s green finance market has developed rapidly, with MAS’s green bond grant scheme, the ASEAN Green Bond Standards, and the sustainability-linked loan frameworks adopted by Singapore’s major banks creating substantial capital available for genuinely green built environment assets. The terms of access to this capital are evolving — and embodied carbon is increasingly part of the conversation.

Green bonds for real estate projects typically require alignment with a recognised taxonomy defining what constitutes a “green” asset. The EU Taxonomy’s technical screening criteria for construction explicitly incorporate lifecycle carbon assessments. Singapore’s domestic frameworks, while currently less prescriptive on embodied carbon, are developing in alignment with international practice under GFIT’s ongoing work. Asset managers who structure green bonds or sustainability-linked loans referencing whole life carbon data — including embodied carbon — are ahead of the regulatory requirement and positioned to access the premium capital that the most rigorous instruments command.

Sustainability-linked loan pricing — where interest rate margins adjust based on verified sustainability performance — provides a direct financial incentive for embodied carbon leadership. A developer who can demonstrate a measured reduction in embodied carbon intensity per square metre of construction, verified against a documented baseline, can structure a sustainability-linked instrument that rewards this performance. Without documented baseline data, this structure is not possible.

The Singapore Building Carbon Calculator (SBCC), developed by NUS-ESI in collaboration with JTC, BCA, and SGBC, provides the calculation methodology that makes embodied carbon verification credible in a Singapore-specific context. Upcyclea’s building passport platform stores and structures the material data that feeds this calculation, creating the audit trail that green finance providers require.

A Practical Pathway for Asset Managers

For asset managers operating in Singapore’s real estate market, the pathway to embodied carbon disclosure capability is sequential but not complex. It requires data, tools, and a connection to the circular material ecosystem that can both deliver verified secondary materials into new construction and extract documented material value from end-of-life assets.

The starting point is material audit. For existing assets, a structured material survey — creating or updating building passport records with current material composition, estimated embodied carbon profiles using SBCC methodology, and end-of-life recovery potential — provides the baseline data from which all subsequent measurement and improvement is referenced. For new developments, the requirement is embedded in design and procurement: EPD-specified materials, SBCC-based carbon budgets, Design for Deconstruction provisions, and building passport creation as a project deliverable alongside the as-built record.

The next step is integration with the circular material ecosystem. For asset managers acquiring or developing Singapore real estate, connection to the Singapore Urban Mine (SUM) platform enables two-way participation: access to verified secondary materials that reduce embodied carbon in new construction, and a pathway for recovering material value from assets being retrofitted or decommissioned. This is not a theoretical circular economy. It is an operational one, with a platform that manages supply, demand, condition verification, and chain of custody documentation.

The disclosure step follows from documentation. With building passport records providing verified material and carbon data, and with the SBCC providing credible emission factor references, portfolio-level embodied carbon disclosure becomes feasible for the first time. This disclosure can be provided to investors through annual sustainability reports, to tenants through lease ESG schedules, to financiers through green finance instrument frameworks, and to regulators through SGX sustainability disclosure.

Singapore’s built environment is at the beginning of the embodied carbon disclosure journey. The infrastructure exists. The regulatory direction is clear. The financial incentives are crystallising. The asset managers who move now are not taking a speculative position. They are building the data capability that will be standard practice within the decade — and capturing the capital market advantage that accrues to those who are ready first.

Upcyclea supports Singapore real estate investors, asset managers, and developers with building passport documentation, embodied carbon accounting, urban mining access, and ESG reporting infrastructure. For portfolio-level implementation or a demonstration of the platform, contact our Singapore team.

References: BCA/SGBC Built Environment Decarbonisation Technology Roadmap (2025); Singapore Green Building Masterplan 4th Edition (2021); MAS Green Finance Industry Taskforce (GFIT) frameworks; Singapore Exchange (SGX) Sustainability Reporting Requirements; SGBC Carbon Resources; Singapore Building Carbon Calculator, NUS-ESI/JTC/BCA/SGBC; SGBC Green Real Estate Trends Conference 2024; TCFD recommendations for real estate.